Articles

Latest

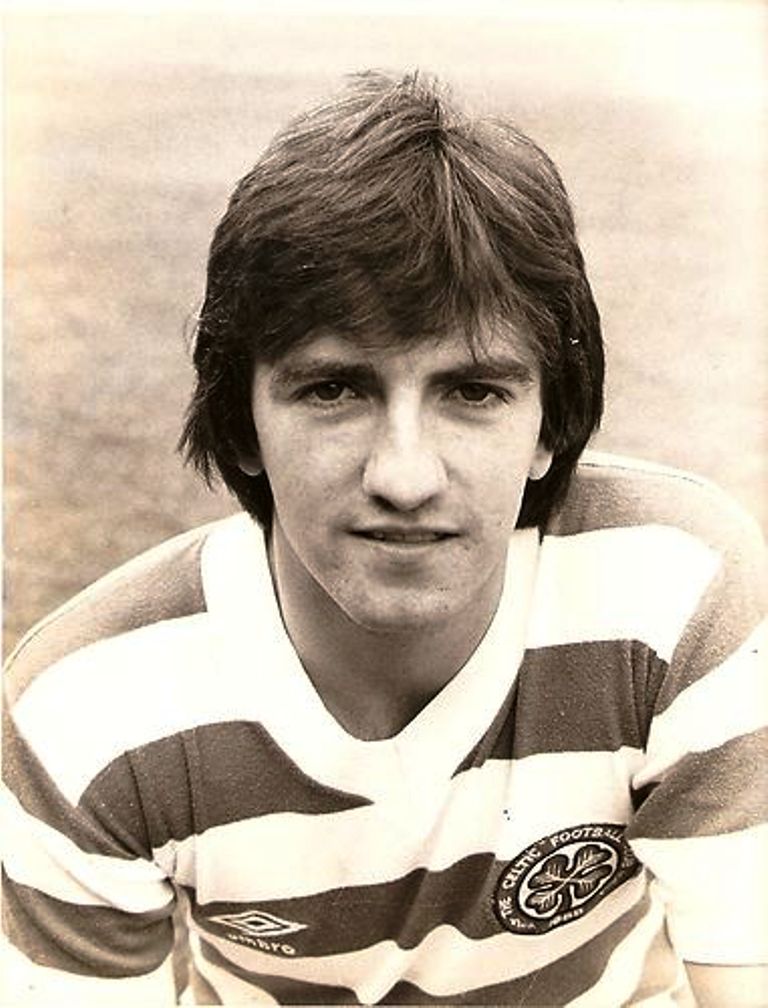

Daniel Kelly. Future captain

Daniel Kelly has all but burst onto the scene for Celtic over the past few weeks. After only...

Multimedia

Latest

I Should Be so Lucky

Once again the lucky bhoys triumphed and Ange won his 3rd out of 4 domestic trophies he has competed for and Bullshit Bingo Beale went home with his tail between his legs.

Podcasts

Podcasts

Latest

I Should Be so Lucky

Once again the lucky bhoys triumphed and Ange won his 3rd out of 4 domestic trophies he has competed for and Bullshit Bingo Beale went home with his tail between his legs.

Video

LatestComing Soon on The Game – Barca 125

The next episode in our podcast series The Game features one of the most iconic matches this...

Images

Latest

Season opener 2022-23

Last Sunday (31st July) saw the flag day season opener of the 2022-23 campaign. Here’s...

- Season 2021-2022

- Season 2020-2021

- Season 2019-2020

- Season 2018-2019

CU REVIEW OF THE SEASON

St Anthony, Harry Brady, Lachie Mor, and Eddie Pearson look back on a successful season for Celtic...

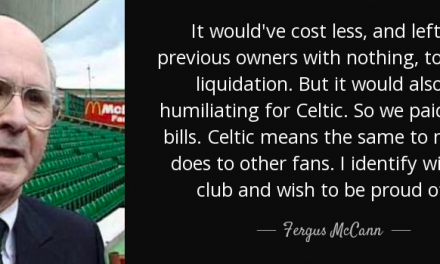

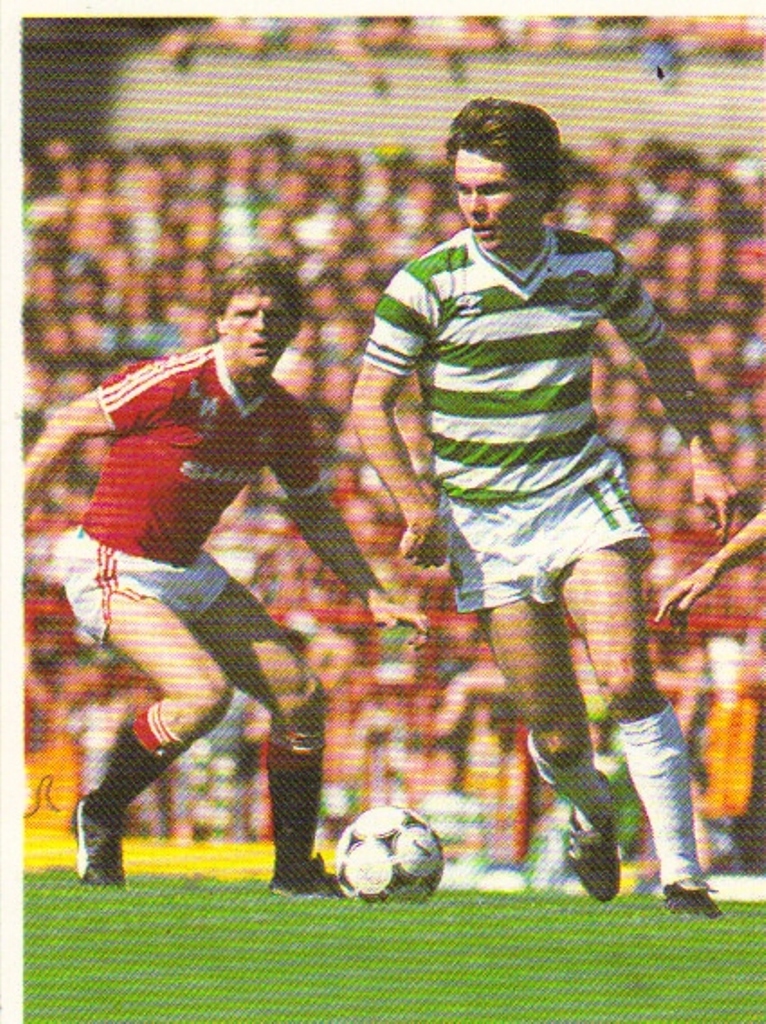

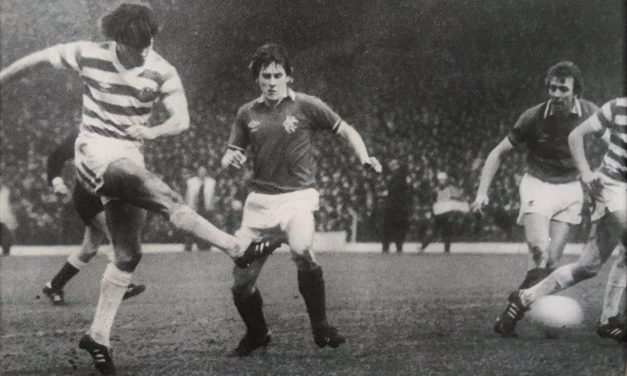

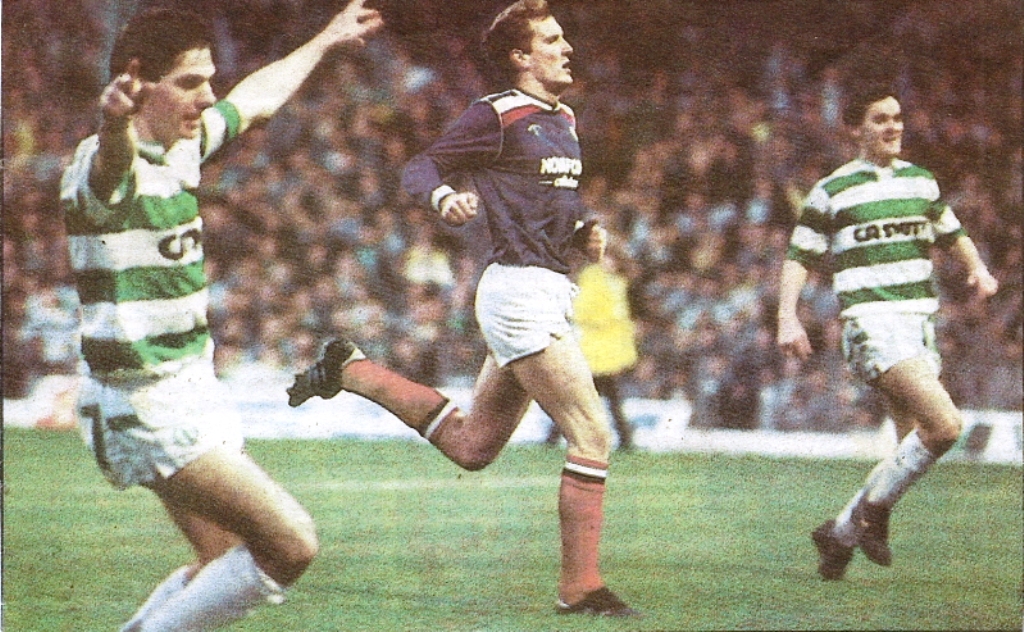

The Millionaire

Today (21 February) marks the 41st anniversary of one of the most remarkable Old Firm (as we...

CELTIC IN THE BLACK AND WHITE ERA – BOOK REVIEW

Review by Joe Bloggs (Celtic Wiki) There’s so many exceptional Celtic books out there from...

The 2018-19 CU Season Review

That was the season that was and what a season, European football past Christmas, a manager going...

- Season 2017-2018

- Season 2016-2017

- Season 2015-2016

- Season 2013-2014

MEMORIES OF EASTER 1981

The year of 1981 did not start well for me. In January I was rushed into hospital for an emergency...

THE ROSENBORG FILES

On Wednesday Celtic take on Rosenborg of Trondheim in a first leg Champions League qualifier at...

DEBUT DAYS – JOE MILLER

14 November 1987 Celtic 5-0 Dundee On the afternoon of Friday 13th of November, Celtic announced...

STUART GRAY: AN APPRECIATION

The very sad news was announced yesterday that ex Celtic player, Stuart Gray, had passed away...

- Season 2012-2013

- Season 2011-2012

- Season 2010-2011

- Season 2009-2010

A Tannadice Memory

When I think of the most memorable games during my time supporting Celtic there are a few obvious...

Scottish Football: Bad Moon Rising

The whole debacle is a series of dry technicalities that have to be explored and explained in...

New Season – It’s Just A Little Too Soon

I sometimes wonder whether the people who run sports just don’t understand fans or pro-actively...

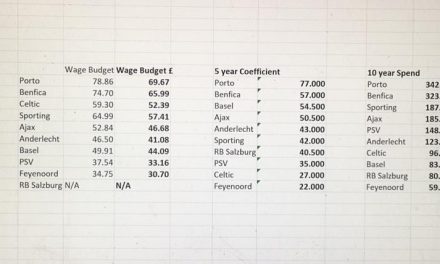

Rich Man, Poor Man, Beggar Man, Thief.

Real Madrid is another example of profligate spending not resulting in success on the field. The...

NEWS NOW

NEWS NOW

- Aberdeen vs Celtic: TV channel, live stream & kick-off time 18/04/2024Aberdeen vs Celtic: TV channel, live stream, team news & kick-off time.

- Leaving Celtic was not a huge consideration for club legend 18/04/2024'Too old & fragile' - Celtic hero says there was no big decision behind leaving the club.

- Clement should stop claiming victories when Rangers don't win 18/04/2024What should concern Philippe Clement more than claiming wins is the true nature of his Rangers team's results.

- Former Celtic manager set for emotional return next month 18/04/2024Former Celtic manager set for emotional return next month.

- 'No money' - Transfer guru names star duo he tried to sign at Celtic 18/04/2024Former Celtic transfer chief Lee Congerton has named the superstar duo he tried to sign at Parkhead as he sighed 'we had no money'.

- Rangers hero admits title race with Celtic is OVER 18/04/2024Kris Boyd makes deflated Rangers title hopes admission after latest slip-up.

- Here is how Celtic could win the league title vs Rangers 18/04/2024The scenario in which Celtic could win the league title vs Rangers.

- Rangers 'handed title back' to Celtic and 'lucky' Rodgers, says pundit 18/04/2024Outspoken pundit Simon Jordan has claimed Rangers have handed the title back to Celtic and 'lucky' Brendan Rodgers.